Creating a budget isn’t just about crunching numbers—it’s about taking control of your life, feeling confident in your financial choices, and turning money stress into money success. When done right, budgeting becomes a tool that frees you rather than chains you to restrictions. Let’s explore the art of creating a budget that actually helps you save money, step by step.

Why Budgeting Matters More Than Ever

Budgeting isn’t just for those trying to pay off debt or stretch a paycheck. It’s a life skill that gives you clarity and freedom. In an era of impulse purchases, subscription traps, and rising costs, understanding where every dollar goes is crucial. Budgeting empowers us to:

- Prioritize savings goals without guilt

- Avoid unnecessary debt

- Reduce financial stress

- Build long-term wealth

Think of it as a roadmap: without it, we’re just wandering through a financial fog, hoping we’ll get somewhere.

Assessing Your Current Financial Picture

Before crafting a budget, we need a clear snapshot of our finances. This includes:

- Income sources: salary, side hustles, investment returns

- Fixed expenses: rent, utilities, insurance

- Variable expenses: groceries, dining out, entertainment

- Debt obligations: loans, credit cards

Tracking this for at least a month reveals spending patterns we often ignore. You’d be surprised how small leaks—like a daily coffee or streaming services we rarely use—add up.

Setting Clear Financial Goals

A budget without purpose is like sailing without a destination. Ask yourself:

- Are we saving for an emergency fund?

- Do we want to pay off debt faster?

- Are we planning for a down payment on a home?

Break goals into short-term (3–6 months), medium-term (1–3 years), and long-term (3+ years). This helps determine how much to allocate toward each.

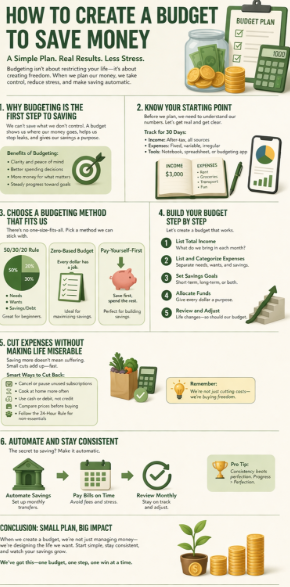

Choosing the Right Budgeting Method

There isn’t a one-size-fits-all approach. Here are some methods to consider:

The 50/30/20 Rule

- 50% for necessities (housing, utilities, groceries)

- 30% for lifestyle choices (dining, entertainment)

- 20% for savings and debt repayment

This method offers flexibility without rigid restrictions.

Zero-Based Budgeting

Every dollar is assigned a purpose—income minus expenses equals zero. This requires more effort but maximizes control over spending and savings.

Envelope System

Cash for each category goes into envelopes. When it’s gone, it’s gone. Perfect for hands-on spenders who need visual boundaries.

Tracking Expenses with Tools and Apps

Budgeting works best when we see real numbers in real time. Modern technology makes this easier:

- Mint – tracks spending automatically across accounts

- YNAB (You Need A Budget) – focuses on planning ahead

- PocketGuard – highlights safe-to-spend amounts

- Spreadsheets – customizable, detailed, and free

The key is consistency. Weekly or daily checks prevent overspending before it spirals out of control.

Categorizing Expenses Effectively

Divide spending into clear buckets to identify where cuts are possible:

- Housing & Utilities

- Transportation

- Food & Dining

- Personal Care

- Entertainment & Hobbies

- Savings & Investments

- Debt Repayment

This structure helps us see opportunities to redirect funds toward savings goals.

Cutting Unnecessary Expenses Without Pain

Budgeting doesn’t mean sacrificing joy—it means smarter spending. Ideas include:

- Cancel unused subscriptions

- Meal prep instead of dining out

- Buy generic brands when possible

- Automate savings to prevent “available cash” temptation

Even small changes—like brewing coffee at home—compound into significant savings over months and years.

Automating Savings for Consistency

Treat savings like a recurring bill. Automating ensures:

- We save before we spend

- No reliance on willpower alone

- Steady progress toward goals

Whether it’s a high-yield savings account, retirement fund, or emergency stash, automation is the silent hero of successful budgeting.

Building an Emergency Fund

Unexpected expenses can derail the best plans. A 3–6 month emergency fund acts as a safety net.

- Start small: $500–$1,000 as an initial buffer

- Gradually increase until fully funded

- Keep it separate from daily spending accounts

Peace of mind from this fund reduces financial stress and prevents debt accumulation.

Tackling Debt Strategically

Debt can be a budget breaker. Approach it methodically:

- Avalanche method: pay off high-interest debt first

- Snowball method: pay off small balances first for motivation

- Avoid accumulating new debt during repayment

Reducing debt frees up funds to redirect into savings and investments.

Adjusting Your Budget Monthly

Budgets aren’t static. Life changes, bills change, and income may fluctuate. Review your budget monthly:

- Did we overspend in any category?

- Are savings contributions on track?

- Are any expenses now unnecessary or outdated?

This iterative approach keeps the budget relevant and actionable.

Incorporating Lifestyle Flexibility

We’re human—rigid budgets often fail because they ignore enjoyment. Include a fun fund:

- Dining out occasionally

- Hobbies and entertainment

- Spontaneous small treats

This prevents “budget burnout” and increases adherence over time.

Prioritizing High-Impact Savings

Not all savings strategies are equal. Consider:

- Refinancing loans for lower interest

- Using cashback or reward programs strategically

- Reviewing insurance policies for potential savings

- Cooking at home versus eating out

High-impact changes may require effort initially but multiply savings quickly.

Using Budgeting to Inform Investment Decisions

Once basic budgeting is solid, we can explore investments:

- Allocate a portion of savings to retirement accounts

- Consider index funds or ETFs for passive growth

- Set aside money for short-term investments like CDs or high-yield accounts

Budgeting gives clarity on how much risk we can afford and ensures investments don’t jeopardize daily financial stability.

Teaching and Involving the Whole Family

A budget works best when everyone’s on the same page:

- Share goals and track progress collectively

- Involve kids in small spending decisions

- Celebrate milestones together

This builds financial literacy and accountability across generations.

Overcoming Budgeting Challenges

Common hurdles include:

- Irregular income

- Overspending on entertainment or dining

- Impulse purchases

Solutions:

- Base the budget on average income for fluctuating earnings

- Set spending limits with alerts

- Delay discretionary purchases for 24 hours to avoid impulse buys

Persistence and flexibility are key.

Monitoring Progress and Celebrating Wins

Budgeting success is measured in progress, not perfection. Celebrate:

- Paying off a credit card

- Hitting a savings milestone

- Reducing monthly expenses

Recognizing achievements reinforces positive habits and motivates continued financial discipline.

Closing Thoughts on Budgeting to Save Money

Creating a budget is less about restriction and more about empowerment. With clarity, automation, and consistent tracking, budgeting transforms from a chore into a life-enhancing practice. We move from surviving paycheck to paycheck to thriving with purpose, ready to tackle short-term needs and long-term dreams.

FAQs

1. How much should I save each month?

Aim for at least 20% of income toward savings and debt repayment. Adjust based on goals and lifestyle.

2. Can I budget with irregular income?

Yes, base your budget on average monthly income and prioritize essential expenses first.

3. Are budgeting apps necessary?

Not mandatory, but they simplify tracking and provide real-time insights that improve adherence.

4. How do I stay motivated to follow a budget?

Set clear goals, automate savings, and reward yourself for achieving milestones.

5. Is it possible to budget and still enjoy life?

Absolutely. Include a fun or leisure fund to maintain balance without derailing savings.