When it comes to borrowing money, we often find ourselves standing at a crossroads. On one side, we have personal loans—quick, flexible, and often unsecured. On the other, mortgages—structured, long-term, and tied to property. So, which one is right for us?

Let’s unpack this together. Think of personal loans as a sprint and mortgages as a marathon. Both get you to a financial destination—but the journey, pace, and risks couldn’t be more different.

Understanding the Basics of Borrowing

Before diving into comparisons, we need to understand what each option actually is.

What Is a Personal Loan?

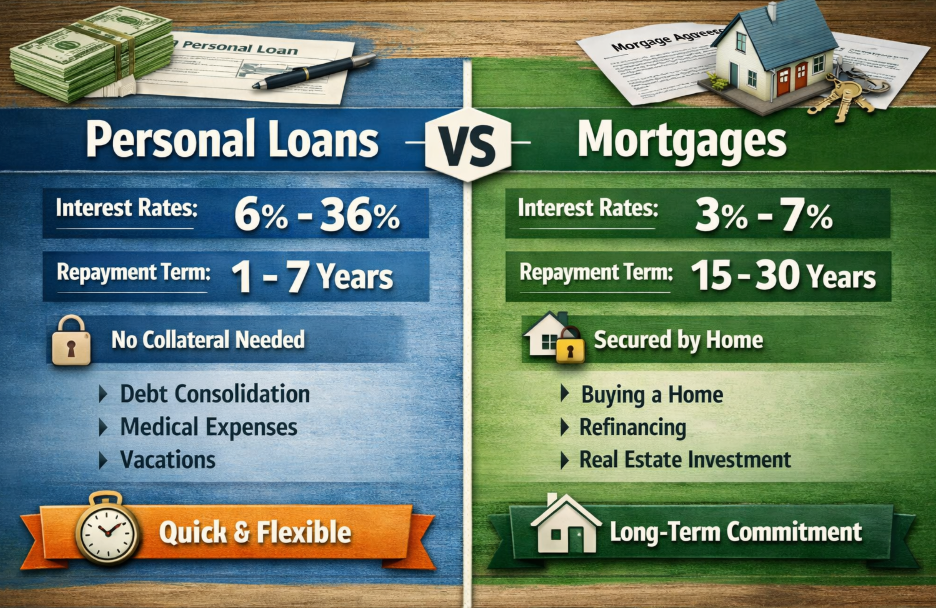

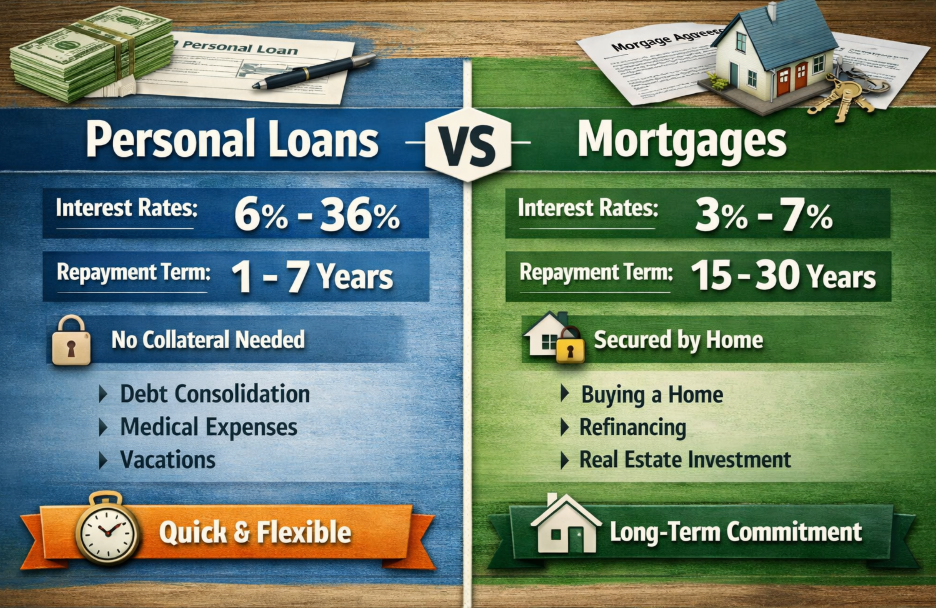

A personal loan is a type of unsecured (sometimes secured) borrowing that we can use for almost anything—medical bills, travel, debt consolidation, or even emergencies.

- Typically ranges from $1,000 to $50,000+

- Short repayment periods (1–7 years)

- Higher interest rates compared to mortgages

- Minimal restrictions on usage

It’s like a financial Swiss army knife—versatile and ready when needed.

What Is a Mortgage?

A mortgage is a secured loan specifically used to purchase or refinance real estate.

- Large loan amounts (often $100,000+)

- Long repayment terms (15–30 years)

- Lower interest rates

- Backed by property as collateral

In simple terms, it’s a long-term commitment tied to your home.

Personal Loans vs Mortgages: The Core Differences

Let’s break down the key differences side by side.

Loan Purpose

- Personal Loans: Flexible use

- Mortgages: Strictly for property

Collateral

- Personal Loans: Usually unsecured

- Mortgages: Secured by the home

Loan Amount

- Personal Loans: Smaller

- Mortgages: Significantly larger

Interest Rates

- Personal Loans: Higher

- Mortgages: Lower

Repayment Terms

- Personal Loans: Short-term

- Mortgages: Long-term

Why Would We Choose a Personal Loan?

Personal loans shine when we need speed and flexibility.

Quick Access to Funds

Sometimes life doesn’t wait. Personal loans can be approved within days—or even hours.

No Collateral Required

We don’t have to risk losing a home or asset.

Flexible Spending

We can use the funds for:

- Medical emergencies

- Travel

- Weddings

- Debt consolidation

Simple Application Process

Less paperwork compared to mortgages.

When Does a Mortgage Make More Sense?

Mortgages are designed for big financial moves—mainly buying property.

Lower Interest Rates

Because they’re secured, lenders offer better rates.

Long-Term Repayment

Monthly payments are more manageable due to extended terms.

Building Equity

Every payment moves us closer to owning an asset.

Interest Rates: The Silent Game-Changer

Interest rates are where things get real.

Personal Loan Rates

- Typically range from 6% to 36%

- Based heavily on credit score

Mortgage Rates

- Usually much lower (e.g., 3%–7%)

- Influenced by market conditions and loan type

Even a small difference in rates can mean thousands over time.

Risk Levels: What’s at Stake?

Personal Loans

- No asset risk (if unsecured)

- But defaulting damages credit

Mortgages

- Risk of foreclosure

- You could lose your home

This is where the emotional weight kicks in. A mortgage isn’t just financial—it’s personal.

Approval Process: Fast vs Thorough

Personal Loan Approval

- Quick credit check

- Minimal documentation

- Fast funding

Mortgage Approval

- Income verification

- Credit history review

- Property appraisal

- Lengthy underwriting process

Mortgages are like a deep background check. Personal loans? More like a quick handshake.

Flexibility vs Structure

Personal Loans Offer Freedom

We decide how to spend the money. No questions asked.

Mortgages Demand Structure

Funds are locked into real estate.

Repayment Terms: Sprint vs Marathon

Personal Loans

- Shorter terms

- Higher monthly payments

Mortgages

- Longer terms

- Lower monthly payments

It’s the difference between ripping off a band-aid and slowly easing into repayment.

Impact on Credit Score

Both loans affect our credit—but differently.

Personal Loans

- Can boost credit if paid on time

- High interest may lead to missed payments

Mortgages

- Strong positive impact over time

- Large debt affects credit utilization

Fees and Hidden Costs

Personal Loans

- Origination fees

- Late payment penalties

Mortgages

- Closing costs

- Appraisal fees

- Insurance and taxes

Mortgages often come with a long list of upfront expenses.

Use Cases: When Each Loan Wins

Best Uses for Personal Loans

- Emergency expenses

- Consolidating high-interest debt

- Short-term financial needs

Best Uses for Mortgages

- Buying a home

- Refinancing property

- Real estate investment

Pros and Cons Breakdown

Personal Loans

Pros:

- Fast approval

- No collateral needed

- Flexible usage

Cons:

- Higher interest rates

- Lower borrowing limits

- Short repayment periods

Mortgages

Pros:

- Lower interest rates

- High loan amounts

- Long repayment terms

Cons:

- Risk of foreclosure

- Complex application process

- Limited use

Choosing the Right Option: A Practical Approach

So how do we decide?

Ask Ourselves These Questions

- What do we need the money for?

- How quickly do we need it?

- Can we handle long-term debt?

- Are we comfortable putting up collateral?

Scenario-Based Decisions

Scenario 1: Emergency Expense

Go with a personal loan—speed matters.

Scenario 2: Buying a House

Mortgage is the only logical option.

Scenario 3: Debt Consolidation

Personal loan works well for combining debts.

Psychological Factors in Borrowing

Let’s be real—money decisions aren’t just logical.

- Personal loans feel less “heavy”

- Mortgages feel like a life milestone

The emotional weight of a mortgage can influence how we perceive risk and commitment.

Long-Term Financial Strategy

Personal Loans as Tools

They help us solve immediate problems.

Mortgages as Investments

They build wealth over time.

Common Mistakes to Avoid

- Taking a personal loan for long-term needs

- Underestimating mortgage costs

- Ignoring interest rates

- Overborrowing

Closing Thoughts: Sprint or Marathon?

At the end of the day, personal loans and mortgages serve completely different purposes.

- Personal loans are fast, flexible, and short-term

- Mortgages are structured, long-term, and asset-based

Choosing between them isn’t about which is better—it’s about which fits our current financial story.

Are we solving a quick problem or building a future?

That’s the real question.

FAQs

1. Can we use a personal loan to buy a house?

Technically yes, but it’s not practical due to low limits and high interest rates.

2. Which is easier to get approved for?

Personal loans are generally easier and faster to obtain.

3. Do mortgages always have lower interest rates?

Yes, because they are secured by property.

4. Can we pay off a mortgage early?

Yes, but some lenders may charge prepayment penalties.

5. Which loan is better for beginners?

It depends—personal loans for small needs, mortgages for long-term investments.